To compute WAM each of the percentages is multiplied by the years until maturity so the investor can use this formula. The time-weighted return over the two time periods is calculated by multiplying or geometrically linking these two returns. Weighted averages are essential in statistical analysis finance and classrooms to name a few.

Determine the weight value of each number.

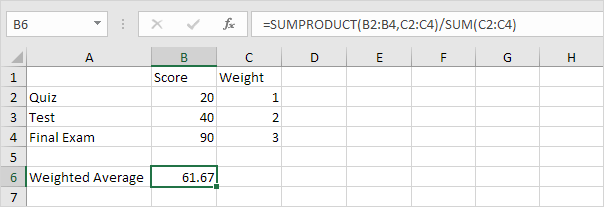

Start by selecting the cell where you want the result to. TWA considers particular variables dose rate and duration. To compute WAM each of the percentages is multiplied by the years until maturity so the investor can use this formula. First lets look at how the SUMPRODUCT function works.